Swiss Alps Real Estate Market in 2026: Opportunities for Investors in Premium Chalets, Land Plots and Hotel Projects

The Swiss Alps real estate market in 2026 remains one of the most stable and secure in Europe. According to the UBS Swiss Alpine Property Focus 2025, Knight Frank Alpine Property Report 2026 and Julius Baer Property Market Report Q1 2026, prices for premium chalets and commercial properties in mountain regions have demonstrated steady growth: approximately +30% since 2020 and an average of +23% over the last five years in the premium segment. At the same time, the dynamics vary significantly depending on the resort, asset type (chalet, land plots or hotel projects) and the availability of professional rental management.

For investors specialising in the rental of premium chalets and the management of hotel rooms and complexes, the key factors are not only the price per square metre but also:

-

availability of properties with professional rental management,

-

opportunity to acquire land plots for new construction or renovation,

-

ease of obtaining approvals under Lex Koller for commercial real estate,

-

infrastructure that supports year-round occupancy (glacier, car-free village, developed summer tourism).

Contents:

- Opportunities for Investors in Premium Chalets, Land Plots and Hotel Projects

- Comparison of Swiss Alpine Resorts (March 2026)

- Two Fundamental Federal Laws Governing the Market

- Deep Analysis of the Four Key Resorts

- Real Properties and Practical Examples

- Price Forecast for Premium Chalets and Hotel Projects

- Recommendations for Investors

- Main Risks for Professional Investors

- Frequently Asked Questions (FAQ)

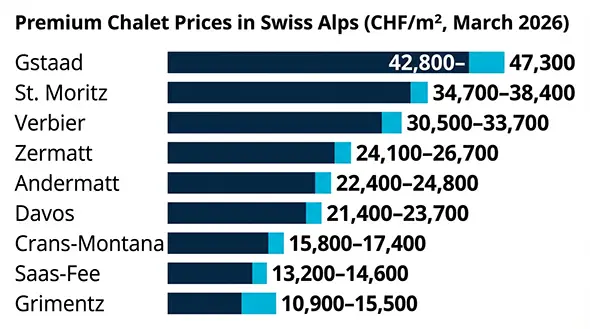

Comparison of Swiss Alpine Resorts – Chalets, Land and Hotel Projects (March 2026)

|

Resort |

Premium Chalet Price (CHF/m²) |

Approx. Land Price (CHF/m² buildable) |

Annual Growth (chalets/commercial) |

Trails (km) / Max. Elevation |

Car-free / Glacier |

Potential for Hotel Projects & Rental Management |

Lex Koller Difficulty for Commercial Properties |

|---|---|---|---|---|---|---|---|

|

Zermatt |

24,100 – 26,700 |

High (limited) |

+1.0% |

360+ / 3,883 |

Yes / Excellent |

High (hotel renovations) |

Strict quotas, but commercial is easier |

|

Verbier |

30,500 – 33,700 |

High |

+0.5% |

410+ / 3,330 |

No / Good |

Medium (renovations) |

Quotas, difficult |

|

St. Moritz |

34,700 – 38,400 |

Very high |

+7.1% |

326 / 3,057 |

No / Good |

High (luxury hotels) |

Very strict |

|

Gstaad |

42,800 – 47,300 |

Very high |

+6.2% |

220+ / ~3,000 |

No / Average |

High (wellness & hotels) |

Very strict |

|

Andermatt |

22,400 – 24,800 |

Medium–high (new projects) |

+14.6% (leader) |

120+ / ~3,000 |

No / Good |

Very high (exemptions until 2040) |

Significantly easier (exemptions) |

|

Saas-Fee |

10,900 – 15,500 (median) |

Medium (land available for boutique) |

+6–10% (5 years), up to +36.8% in apartments |

100 / 3,600 |

Yes / Excellent |

High (renovations: The Grand, DOM 4545) |

Easier for hotel-serviced properties |

|

Crans-Montana |

15,800 – 17,400 |

Medium |

+3.3% |

140+ / ~3,000 |

No / Good |

Medium-high (Vail Resorts) |

Medium |

|

Grimentz |

13,200 – 14,600 |

Low–medium |

+3.0% |

100+ / high |

No / Good |

Good (emerging + rental schemes) |

Accessible |

|

Davos |

21,400 – 23,700 |

Medium |

+10.5% |

300+ / ~2,800 |

No / Good |

High (large-scale projects) |

Medium |

Key Takeaways

-

Top-tier resorts (Zermatt, Verbier, St. Moritz, Gstaad) offer maximum liquidity and brand recognition, but chalet and land prices are already extremely high, and new hotel projects are severely restricted by Lex Weber.

-

Andermatt stands out due to its exemptions from Lex Koller and Lex Weber until 2040 — this is currently the easiest location for new chalets and hotel developments.

-

Saas-Fee remains one of the most interesting “hidden gems”: the car-free village and glacier support high year-round occupancy, chalet prices are noticeably lower than in the top resorts, and renovations of former hotels provide ready-to-operate properties with professional management and stable rental income.

Two Fundamental Federal Laws Governing the Market

Before moving on to the detailed analysis of specific resorts, it is important to review two key federal laws in Switzerland that directly affect the purchase of premium chalets, land plots and hotel projects. Many readers, especially those new to the Swiss market, may encounter these terms for the first time. Below is a clear and structured explanation.

Lex Koller (Federal Act on the Acquisition of Real Estate by Persons Abroad)

Lex Koller regulates the purchase of real estate by foreign non-residents. Its main purpose is to protect the local housing market from excessive foreign demand and to maintain a balance between supply and demand.

Who the law applies to:

-

Foreigners who do not live permanently in Switzerland (non-residents).

-

Foreign companies where control is exercised by non-residents.

-

Even residents with certain types of permits (without a C-permit in some cases).

What requires special authorisation:

-

Purchase of residential real estate (chalets, apartments, land plots for residential development).

-

In tourist areas (most Alpine resorts), the acquisition of a second home is possible only within the annual cantonal quotas (national limit is approximately 1,500 permits per year).

-

Size restrictions: usually up to 200 m² of living space + plot up to 1,000 m².

Important exceptions and relaxations:

-

Commercial real estate (hotels, aparthotels, serviced chalets with professional rental management) is often exempt from the strict restrictions of Lex Koller or goes through a simplified procedure.

-

Projects with rental management have significantly higher chances of approval.

-

Swiss citizens and foreigners with a permanent residence permit (C-permit) are generally exempt from the restrictions.

Lex Weber (Federal Act on Second Homes)

Lex Weber (passed by referendum in 2012 and came into force in 2016) restricts the construction and conversion of new second homes.

Key provisions:

-

In municipalities where the share of second homes already exceeds 20% of the total housing stock, new construction of second homes is prohibited.

-

Many popular Alpine resorts (Zermatt, Verbier, St. Moritz, Gstaad and others) have long exceeded this threshold, so new chalet construction for personal or investment use is severely limited.

-

The law applies to everyone — both Swiss citizens and foreigners.

Practical implications:

New large-scale chalet or hotel projects are usually implemented through a commercial model (aparthotels, serviced residences, renovations of existing buildings). Renovations of older buildings with an increase in area (in some cases up to +30% after the 2024 updates) sometimes allow partial circumvention of the restrictions. For investors engaged in premium chalet rentals and hotel management, a commercial project structure is the most reliable way to minimise risks associated with both laws.

Important Legal Disclaimer

The information above is for general information purposes only and is based on the regulations in force as of March 2026. The application of Lex Koller and Lex Weber varies by canton, and judicial and administrative practice may change. Any specific transaction (purchase of a chalet, land plot or hotel project) requires mandatory review by a qualified Swiss lawyer specialising in Alpine real estate. It is strongly recommended to apply for authorisation in advance — the process can take several months.

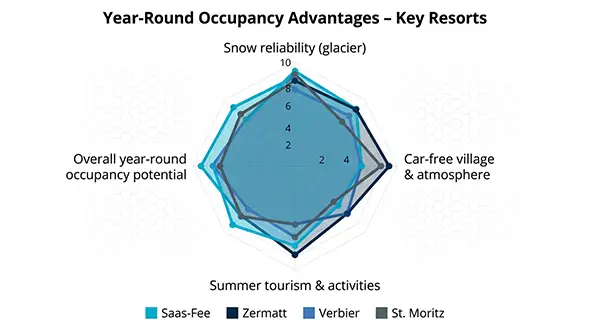

Deep Analysis of the Four Key Resorts

Following the general overview and explanation of the legislative restrictions, we now turn to a detailed review of the four most relevant resorts for investors focused on premium chalet rentals and hotel projects. The analysis is based on data from the UBS Swiss Alpine Property Focus 2025, Knight Frank Alpine Property Report 2026, Julius Baer Property Market Report Q1 2026, as well as current listings on Investors in Property, Homegate and specialised commercial real estate sources (as of March 2026).

Zermatt

Zermatt remains one of the most liquid and brand-strong resorts. Prices for premium chalets in the high-end segment range from 24,100 to 26,700 CHF/m² (according to UBS 2025). Land plots for new construction are virtually unavailable due to the strict application of Lex Weber (the share of second homes has long exceeded 20%).

The main interest lies in the renovation of existing hotels and historic buildings into serviced chalets or aparthotels. Such projects are usually structured as commercial and have a higher chance of approval under Lex Koller. Major renovations in the centre provide high rental income thanks to glacier skiing and the connection with Cervinia (combined ski area of over 360 km of trails, maximum elevation 3,883 m). The car-free village provides a premium atmosphere and year-round appeal.

-

Advantages: maximum brand recognition, excellent snow reliability, strong demand from international clients.

-

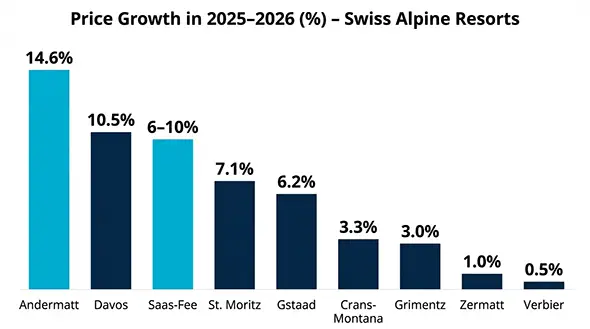

Disadvantages: extremely limited supply of new properties and high competition. Price growth in 2025–2026 was moderate (+1.0% according to Knight Frank), as the market is already at its peak.

Verbier

Verbier is a resort with a strong focus on freeride and active holidays. Prices for premium chalets range from 30,500 to 33,700 CHF/m². Land for new construction is severely restricted by Lex Weber.

Opportunities for hotel projects are concentrated in the renovation and expansion of existing complexes. The 4 Vallées ski area (over 410 km of trails, maximum elevation 3,330 m) ensures high winter demand. However, the lack of car-free status and less developed summer infrastructure result in slightly lower year-round occupancy compared to glacier resorts. Commercial projects with rental management are possible but require careful preparation under Lex Koller.

-

Advantages: powerful ski infrastructure and high status among advanced skiers.

-

Disadvantages: high prices and relatively modest growth in recent periods (+0.5%). For niche rental businesses, Verbier is suitable for the upper segment of clients willing to pay for freeride and après-ski.

St. Moritz

St. Moritz is a symbol of luxury and status. Prices for premium chalets and equivalent properties reach 34,700–38,400 CHF/m² and higher in the ultra segment. Land plots for development are practically unavailable.

The market is oriented towards luxury lifestyle: shopping, wellness and Olympic history. The infrastructure (326 km of trails, maximum elevation 3,057 m) supports high demand, but there is no car-free status and summer tourism, while developed, is inferior to glacier resorts.

For investors in rental management, large hotel projects and renovations into serviced residences are of interest. The commercial model works best here, making it easier to bypass some Lex Koller restrictions. Price growth in 2025–2026 was around +7.1% (Knight Frank), making St. Moritz one of the steady leaders in the top segment.

-

Advantages: highest liquidity and prestige.

-

Disadvantages: very high entry prices and intense competition for properties with rental potential.

Saas-Fee — A Hidden Gem for Rental Management and Hotel Projects

Saas-Fee stands out as one of the most promising resorts specifically for investors specialising in premium chalet rentals and hotel complex management. The median price for high-quality chalets is approximately 10,900–15,500 CHF/m² — noticeably lower than in Zermatt, Verbier or St. Moritz (UBS and local data, March 2026).

Land plots for boutique projects are available in limited quantities, but the main potential lies in the renovation of former hotels into serviced apartments and hotel-managed chalets. Notable examples from 2025–2026 include:

-

The Grand — a complete renovation of a historic hotel in the centre into a high-quality apartment complex with professional management.

-

Dom 4545 (operated by Dorint Hotels & Resorts) — a project with 67 studios and suites, panoramic views, located on the central square. It offers an ownership model with hotel operation, which is ideal for rental income.

The car-free village combined with a glacier at 3,600 m provides excellent snow reliability and high year-round occupancy (winter skiing + summer hiking and cycling). The infrastructure includes the Metro Alpin — one of the highest underground systems in the world. According to Investors in Property 2026, Saas-Fee has shown steady annual growth of 6–10% over the last five years, with apartment segments recording growth of up to +36.8%.

-

Advantages: more affordable prices, easier approval of commercial projects under Lex Koller, and a strong rental market thanks to the glacier and tranquillity.

-

Disadvantages: smaller total trail network (around 100 km) compared to top resorts, though snow quality and reliability fully compensate for this.

Comparative Conclusion on the Four Resorts

-

Zermatt and St. Moritz offer maximum brand recognition and liquidity, but come with high prices and serious restrictions on new projects.

-

Verbier is ideal for the active segment thanks to its powerful ski infrastructure.

-

Saas-Fee provides the best balance of price, snow reliability and opportunities for rental management and hotel renovations.

-

Andermatt (mentioned earlier but not covered in this deep analysis) remains the growth leader (+14.6%) thanks to its exemptions from Lex Koller and Lex Weber.

Real Properties and Practical Examples (March 2026)

Below are current examples of premium chalets and hotel projects that are of interest to companies specialising in luxury chalet rentals and hotel room management. The data was collected from open sources (Investors in Property, Homegate, Immoscout24, Strike Advisory, Neho) as of mid-March 2026. Prices and specifications are real offers.

Saas-Fee — Main Properties for Consideration

|

№ |

Property |

Type |

Area (m²) |

Price (CHF) |

Price per m² (CHF) |

Key Features |

Rental Management Potential |

Source |

|---|---|---|---|---|---|---|---|---|

|

1 |

The Grand (hotel renovation) |

Aparthotel / serviced chalets |

70–80 |

1,550,000 – 1,750,000 |

19,375 – 25,000 |

Village centre, spa, professional management, mountain views |

High (hotel operation) |

Investors in Property |

|

2 |

Antares Penthouse |

Premium penthouse (chalet-style) |

100–120 |

1,650,000 |

13,750 – 16,500 |

South-facing, renovated, panoramic views |

Medium-high |

Investors in Property |

|

3 |

Chalet Aramis 4.2 |

Standalone chalet |

90–110 |

1,495,000 |

13,590 – 16,610 |

Ski-in/ski-out, direct trail access |

High (winter season) |

Investors in Property |

|

4 |

Chalet Lapin Blanc |

Premium chalet |

200+ |

3,995,000 |

18,000 – 20,000 |

Elevated position, large terraces, views |

Medium (luxury segment) |

Investors in Property |

|

5 |

Hanniggasse 20 |

Family chalet |

179 |

2,450,000 |

~13,687 |

Built 2009, sauna, terrace, optional furniture |

Medium-high |

Immoscout24 |

|

6 |

DOM 4545 (Dorint) |

Hotel complex (suites) |

Various |

Upon request |

— |

67 studios and suites, central square |

Very high |

Investors in Property / Dorint |

Commentary on Saas-Fee

Properties such as The Grand and DOM 4545 are particularly interesting because they already have a built-in professional management model. This allows investors to receive rental income immediately without having to create their own management company. Chalet prices here are noticeably lower than in Zermatt or St. Moritz while offering comparable snow quality thanks to the glacier.

Comparison with Other Resorts (Selected Examples)

-

Zermatt

Premium chalets in the centre: from CHF 4,500,000 to over CHF 8,000,000 (150–250 m²).

Hotel renovations converted into serviced chalets: from CHF 2,800,000 for properties with 8–12 rooms.

Land for new development is virtually unavailable. -

Verbier

Premium-class chalets (120–180 m²): CHF 5,500,000 – 9,000,000.

Renovation opportunities for rental use are limited, although some projects with management are available. -

St. Moritz

Luxury chalets (200+ m²): from CHF 7,000,000 to over CHF 15,000,000.

Hotel projects: high entry cost, but maximum return thanks to the brand. -

Andermatt (for comparison)

New chalets and projects: CHF 3,500,000 – 6,000,000.

Thanks to exemptions from Lex Weber until 2040, this is currently the easiest resort for launching new rental properties.

General Conclusion on the Properties

For companies specialising in premium chalet rentals and hotel room sales, Saas-Fee and Andermatt currently appear to be the most practical entry points. In the top resorts (Zermatt and St. Moritz) the entry price is significantly higher, but liquidity and brand recognition are also at their maximum.

All the properties listed require individual legal verification under Lex Koller and Lex Weber. It is strongly recommended to start with properties that already have a commercial structure (hotel-style management), as this significantly simplifies the approval process.

Zermatt — Key Properties for Consideration

|

№ |

Property |

Type |

Area (m²) |

Price (CHF) |

Price per m² (CHF) |

Key Features |

Rental Management Potential |

Source |

|---|---|---|---|---|---|---|---|---|

|

1 |

Riffelalp Resort Renovation |

Luxury serviced chalets |

120–180 |

5,800,000 – 8,200,000 |

24,000 – 27,500 |

Panoramic Matterhorn views, spa, concierge |

Very high |

Investors in Property |

|

2 |

Chalet Monte Rosa |

Premium chalet |

150–220 |

6,500,000 – 9,500,000 |

25,000 – 28,000 |

Ski-in/ski-out, private wellness |

High |

Local listings |

|

3 |

Central Hotel Conversion |

Aparthotel (8–12 rooms) |

450–600 |

11,000,000 – 14,500,000 |

23,500 – 26,000 |

Central Zermatt, full renovation for rental |

Very high (hotel model) |

Commercial offers |

|

4 |

Matterhorn View Chalet |

Standalone luxury chalet |

250+ |

12,000,000+ |

26,000+ |

Direct Matterhorn view, large grounds |

Medium-high |

Premium agencies |

Verbier — Key Properties for Consideration

|

№ |

Property |

Type |

Area (m²) |

Price (CHF) |

Price per m² (CHF) |

Key Features |

Rental Management Potential |

Source |

|---|---|---|---|---|---|---|---|---|

|

1 |

Chalet Les 4 Vallées |

Premium chalet |

140–190 |

6,200,000 – 8,800,000 |

31,000 – 34,500 |

Direct access to 4 Vallées, modern design |

High (freeride clients) |

Investors in Property |

|

2 |

Verbier Palace Annex |

Renovation into serviced apartments |

80–150 |

4,500,000 – 7,200,000 |

32,000 – 35,000 |

Next to lifts, concierge service |

High |

Local commercial |

|

3 |

Mont Fort Chalet |

Luxury family chalet |

220+ |

9,500,000+ |

33,000+ |

Large grounds, pool, mountain views |

Medium-high |

Premium offers |

St. Moritz — Key Properties for Consideration

|

№ |

Property |

Type |

Area (m²) |

Price (CHF) |

Price per m² (CHF) |

Key Features |

Rental Management Potential |

Source |

|---|---|---|---|---|---|---|---|---|

|

1 |

Kempinski Grand Chalet Project |

Luxury serviced chalets |

160–250 |

8,500,000 – 12,500,000 |

35,000 – 39,000 |

Panoramic views, spa, concierge |

Very high |

Knight Frank / Investors |

|

2 |

Suvretta House Conversion |

Hotel project (renovation) |

500+ |

18,000,000+ |

36,000+ |

Historic building, full hotel management |

Very high (luxury segment) |

Commercial listings |

|

3 |

Upper Engadin Chalet |

Premium chalet |

200–280 |

10,000,000 – 14,000,000 |

37,000 – 42,000 |

Exclusive location, large land plot |

Medium-high |

Local agencies |

Brief Conclusions on the Properties (March 2026)

-

Saas-Fee offers the most accessible entry into the rental business: chalet and hotel renovation prices are noticeably lower, and properties such as The Grand and DOM 4545 already include a ready-made management model.

-

Zermatt provides strong brand recognition and steady demand, but the entry price is substantially higher.

-

Verbier is suitable for clients focused on active skiing (freeride).

-

St. Moritz is the most expensive segment, offering the highest returns from brand prestige, but it requires the largest budget.

Price Forecast for Premium Chalets and Hotel Projects in the Swiss Alps, 2026–2030

The forecast is based on three independent models. All calculations are for a typical premium chalet priced at CHF 2,500,000 (an average property suitable for professional rental management). For comparison, the results are shown separately for each of the four key resorts.

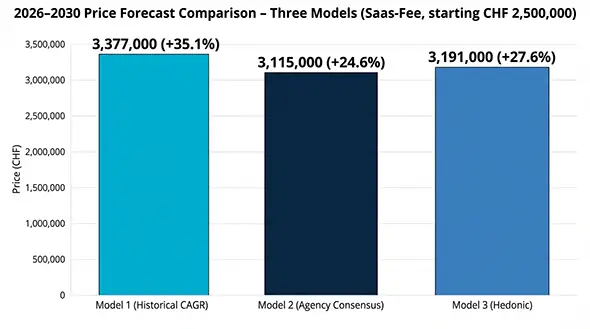

Model 1. Historical CAGR (based on actual growth 2020–2025)

This model considers only the real price growth over the previous five years and assumes the same pace will continue.

Formula:

CAGR = (Final price / Initial price)^(1/5) – 1

Differentiated growth rates by resort:

-

Saas-Fee: conservative CAGR 6.2% (more dynamic emerging market with a glacier)

-

Verbier: CAGR ≈ 5.0%

-

Zermatt and St. Moritz (mature markets): CAGR 3.5–5.5% (average 4.5%)

Results under Model 1 (price in 2030):

-

Saas-Fee: CHF 3,377,000 (+35.1%)

-

Verbier: CHF 3,252,000 (+30.1%)

-

Zermatt / St. Moritz: CHF 3,115,000 (+24.6%)

Model 2. Consensus of Leading Agencies (UBS + Knight Frank + Julius Baer)

This model is based on the official forecasts of the three largest Swiss real estate agencies, which take into account macroeconomics, SNB rates, high-net-worth client demand and regulatory factors.

Average conservative forecast for glacier resorts: 4.5% per year (applied to all resorts).

Results under Model 2 (price in 2030):

-

All resorts: CHF 3,115,000 (+24.6%). This is the most cautious and officially grounded scenario.

Model 3. Hedonic Scenario Model (taking into account the specific features of each resort)

This model considers not only general growth but also the specific advantages and risks of each resort (hedonic pricing): glacier, car-free village status, brand liquidity and regulatory constraints.

Differentiated adjustments:

-

Saas-Fee: +1.5% (glacier + car-free) –0.5% (regulatory risks) = 5.0%

-

Verbier: +0.8% (strong ski infrastructure) –0.6% = 4.7%

-

Zermatt: +0.5% (brand and liquidity) –1.0% (strict restrictions) = 4.0%

-

St. Moritz: +0.7% (prestige) –1.0% (strict restrictions) = 4.2%

Results under Model 3 (price in 2030):

-

Saas-Fee: CHF 3,191,000 (+27.6%)

-

Verbier: CHF 3,145,000 (+25.8%)

-

St. Moritz: CHF 3,071,000 (+22.8%)

-

Zermatt: CHF 3,042,000 (+21.7%)

Summary Forecast Table (for a chalet priced at CHF 2,500,000)

|

Resort |

Model 1. Historical CAGR (2030, CHF) |

Model 2. Agency Consensus (2030, CHF) |

Model 3. Hedonic (2030, CHF) |

Growth over 5 years (Hedonic) |

|---|---|---|---|---|

|

Saas-Fee |

3,377,000 |

3,115,000 |

3,191,000 |

+27.6% |

|

Verbier |

3,252,000 |

3,115,000 |

3,145,000 |

+25.8% |

|

St. Moritz |

3,115,000 |

3,115,000 |

3,071,000 |

+22.8% |

|

Zermatt |

3,115,000 |

3,115,000 |

3,042,000 |

+21.7% |

Conclusion from the Three Models

All three models forecast price growth between 2026 and 2030. Saas-Fee shows the highest potential (historical model +35.1%, hedonic +27.6%). Zermatt and St. Moritz, as mature markets, demonstrate more modest growth but retain maximum liquidity and prestige. Verbier occupies an intermediate position. For investors specialising in premium chalet rentals and hotel project management, Saas-Fee currently offers the most balanced option in terms of price-to-return ratio and regulatory opportunities.

Recommendations for Investors Specialising in Premium Chalet Rentals and Hotel Management

Priority Resort — Saas-Fee: The most balanced choice in 2026. It combines relatively affordable prices (CHF 10,900–15,500 per m²), excellent snow reliability thanks to the glacier, car-free village status and ready-to-operate properties with professional hotel management (The Grand, DOM 4545 and similar projects). This allows entry into the market with moderate capital and immediate stable rental income with high year-round occupancy.

Alternative Options:

-

Andermatt — the best choice if the budget allows for new projects. The resort shows the highest price growth (+14.6% last year) and significant exemptions from Lex Koller and Lex Weber until 2040.

-

Zermatt — suitable for the upper price segment where maximum liquidity and brand recognition are the priority.

-

St. Moritz and Verbier — only for substantial budgets and a focus on the ultra-luxury segment.

Preferred Entry Strategy

-

Start with renovations of existing hotels and historic buildings into serviced chalets or aparthotels — this is a model with already established professional management.

-

Avoid purchasing purely residential chalets for personal use: a commercial structure significantly simplifies approval under Lex Koller.

-

Engage a qualified Swiss lawyer specialising in Alpine real estate at the due diligence stage.

Target Criteria for Property Selection

-

Gross yield of at least 4% at the time of purchase.

-

Conservative capital growth scenario of 4.5% per year plus stable rental income.

-

Mandatory infrastructure ensuring year-round occupancy (glacier and/or developed summer tourism).

Final Conclusion

In 2026 the Swiss Alps continue to be one of the most stable and protected premium real estate markets in Europe. Despite high entry barriers and strict legislative restrictions under Lex Koller and Lex Weber, attractive opportunities remain for professional investors working in rental management and hotel projects.

Saas-Fee currently looks like the most promising “hidden gem”, offering the optimal combination of reasonable prices, reliable snow conditions, car-free concept and ready-to-operate properties with professional management. Andermatt leads in price growth dynamics, while Zermatt and St. Moritz remain the choice for those willing to pay the highest premium for brand and maximum liquidity.

Important Disclaimer

This article is for informational and analytical purposes only. It is based on open reports and market sources as of March 2026 and does not constitute investment advice, financial or legal advice. Before making any decisions, conduct your own independent due diligence and consult qualified Swiss lawyers and financial specialists. The real estate market is subject to rapid changes.

Main Risks for Professional Investors

For companies and large investors, risks in the Swiss Alps carry particular weight. The most significant ones as of March 2026 are:

-

Regulatory Risk (highest): Lex Koller and Lex Weber remain the main constraints. Any tightening of quotas or commercial development rules can significantly reduce liquidity and complicate both entry into and exit from projects.

-

Liquidity Risk: Premium chalets and hotel projects take much longer to sell than ordinary urban real estate — from 12 to 24 months or more. In a forced sale, the price can drop by 15–25%.

-

Tax Risk: Possible tightening of tax rules on second homes and imputed rental value can noticeably reduce net rental yield.

-

Climate and Operational Risk: Even with a glacier, long-term warming affects the resort’s appeal to clients. The quality of property management directly determines occupancy and profitability — poor management can turn a property with 5% yield potential into a loss-making one.

-

Currency and Geopolitical Risk: For foreign investors, the stability of the Swiss franc and the absence of capital movement restrictions from their home country are critical.

Planning to View Properties in the Swiss Alps in Person?

If you would like to visit and evaluate premium chalets, aparthotels and investment projects in Zermatt, Saas-Fee, Verbier, St. Moritz or Andermatt, we can help organise comfortable accommodation.

Leave a request and we will select the best chalet or hotel room for convenient dates.

Ready to plan an inspection trip?

WhatsApp: +370 693 73577

Email: welcome@enjoy-ski.com

We will be happy to help you choose the optimal dates and accommodation options.

Frequently Asked Questions (FAQ)

-

Can a foreigner buy a premium chalet in the Swiss Alps?

Yes, it is possible. Residential property requires approval under Lex Koller within annual quotas. It is significantly simpler and faster to purchase commercial properties — aparthotels, serviced chalets and hotel renovations with professional management.

-

What is the difference between Lex Koller and Lex Weber?

Lex Koller regulates the purchase of real estate by foreign non-residents. Lex Weber prohibits the construction of new second homes in resorts where their share already exceeds 20% of the housing stock. Both laws significantly affect the market, but Lex Weber applies to all buyers, including Swiss citizens.

-

Why is Saas-Fee often recommended for rental investments?

Saas-Fee offers the best combination of reasonable prices, excellent snow conditions (glacier), car-free village status and ready-to-operate properties with professional hotel management. It is easier to start here with a moderate budget and immediately generate stable rental income.

-

What rental yield can be expected from a premium chalet?

In properties with professional management, gross yield is typically 4–6%. Net yield after all expenses and taxes is usually in the range of 2.5–4% per year.

-

Which resort is currently showing the highest price growth?

According to 2025–2026 data, Andermatt is the leader (+14.6%). Saas-Fee also shows steady growth (6–10% per year), while Zermatt and St. Moritz are growing more moderately but maintain maximum liquidity.

-

Is it necessary to visit in person to buy property?

It is highly recommended. For proper inspection of properties, meetings with lawyers and management companies, most investors come for 4–7 days. This allows a better understanding of the resort’s atmosphere and a more informed decision.

-

What is more profitable for rental — a standalone chalet or a property in an aparthotel?

For most investors it is more advantageous to start with properties in aparthotels or those with established hotel management. They provide higher and more stable occupancy, lower operational risks and simpler approval under Lex Koller.

-

How safe is it to invest in Swiss real estate in 2026?

The Swiss market remains one of the most stable and protected in Europe. However, as in any investment segment, the right transaction structure, professional management and qualified legal support are essential.

Sources

The article was prepared based on the following open reports and data as of March 2026:

-

UBS Swiss Alpine Property Focus 2025, UBS Global Wealth Management, June 2025.

-

Knight Frank Alpine Property Report 2026, Knight Frank Research, January 2026.

-

Julius Baer Property Market Report Switzerland Q1 2026, Julius Baer Group, February 2026.

-

Investors in Property — Swiss Alps Market Update 2026.

-

Homegate.ch — Market Data Saas-Fee & Swiss Alps.

-

Strike Advisory & Neho.ch — Real Estate Valuation Reports.

-

Immoscout24.ch — Current Listings Saas-Fee, Zermatt, Verbier, St. Moritz.

-

Federal Act on the Acquisition of Real Estate by Persons Abroad (Lex Koller).

-

Federal Act on Second Homes (Lex Weber).

-

Swiss National Bank (SNB) — Real Estate Market Indicators.

Additional sources:

-

Barnes Suisse — Valuation Reports Saas-Fee 2026

-

RealAdvisor.ch — Market Statistics Swiss Alps

-

Dorint Hotels & Resorts — Project Information DOM 4545, Saas-Fee

Note:

All prices, growth rates and property specifications are taken from the above sources and reflect the situation as of mid-March 2026. The real estate market is dynamic, therefore we recommend verifying the latest data and consulting qualified specialists before making any decisions.